Read Hyundai’s official statement on its new, complete ownership of Boston Dynamics closely enough, and something odd turns up near the bottom: a two-line glossary. The company felt the need to explain, for the benefit of reporters, what a “put option” is and what a “call option” is. That’s not the kind of detail a company includes when it wants credit for a bold strategic move. It’s the kind of detail a company includes when it wants you to understand why it didn’t really have a choice.

Garage-worthy EDC gear, on sale this week.

On July 16, Hyundai Motor Group confirmed it is acquiring SoftBank’s remaining 9.65 percent stake in Boston Dynamics, making the robotics maker a wholly owned subsidiary for the first time since Hyundai bought control of it back in 2020. The move wasn’t triggered by a sudden burst of confidence inside Hyundai’s boardroom. It was triggered by SoftBank, which exercised a put option written into the original deal, a contractual mechanism that let SoftBank force Hyundai’s side of the table to buy them out on terms set five years ago, not terms negotiated today.

Financial outlets in Korea and internationally have pegged the price at somewhere between $325 million and roughly $337 million, depending on the exchange rate used. That number matters less than what it implies: a company-wide valuation for Boston Dynamics of about $3.4 billion, roughly three times the $1.1 billion price tag Hyundai paid for control in 2021. Boston Dynamics hasn’t shipped a mass-market product in that stretch. What changed is the market’s appetite for anything wearing the label humanoid robotics.

Here’s a detail most coverage of this deal skipped entirely. Hyundai buying Boston Dynamics has never meant one single corporate entity writing one single check. The 2020 purchase split the 80 percent stake among Hyundai Motor Company, Kia, Hyundai Mobis, Hyundai Glovis, and, this is the part worth sitting with, Executive Chair Euisun Chung personally, who holds roughly 22.6 percent of the robotics company in his own name, according to Korean financial press. That’s a bigger individual stake than either Kia or Glovis holds. A car company’s chairman personally owning close to a quarter of its robotics subsidiary is the kind of governance wrinkle that would draw real scrutiny at almost any other public company. At Hyundai, it’s a footnote.

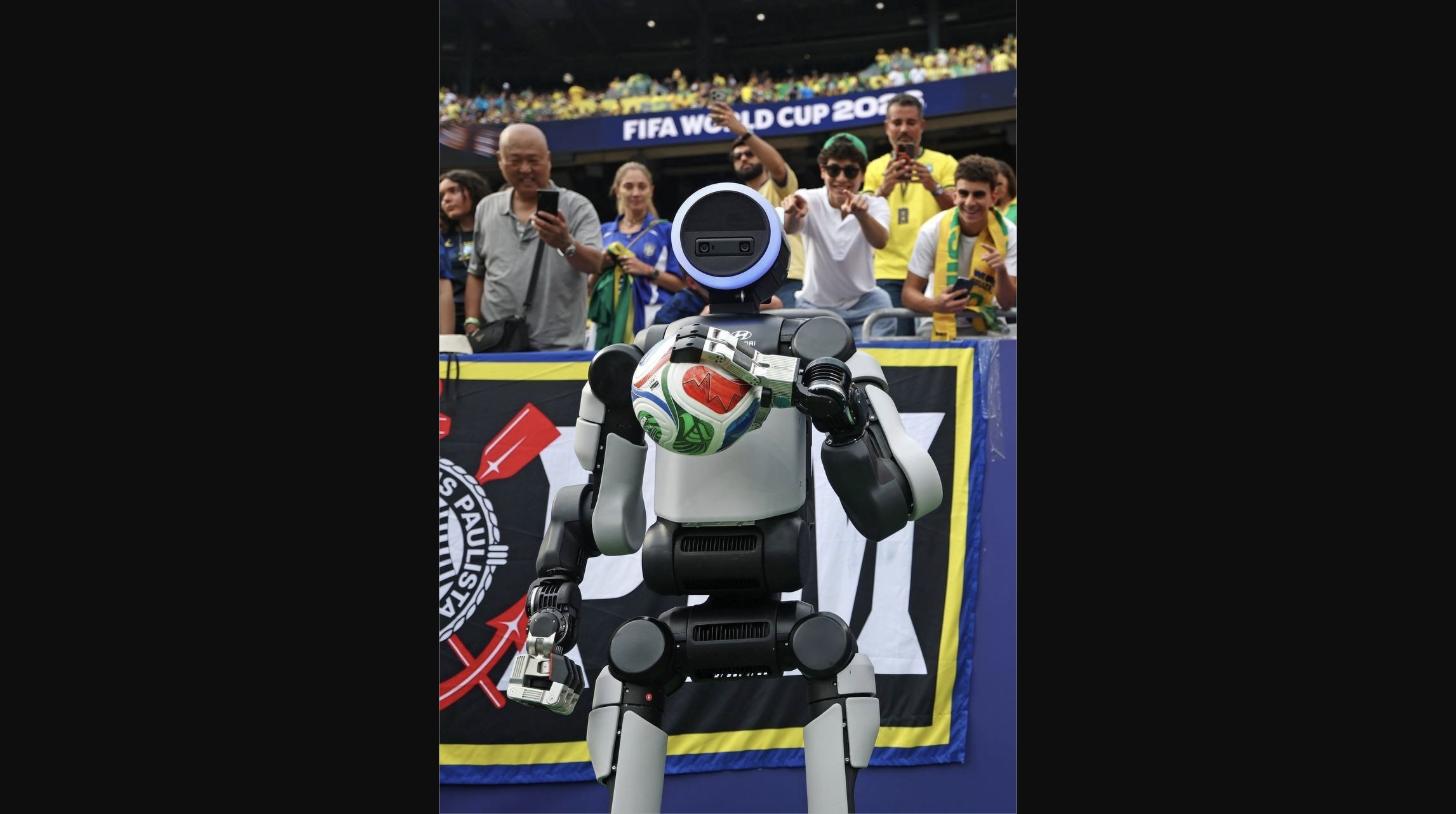

The more consequential misunderstanding is about what Atlas is actually going to do. Hyundai’s own statement is specific, and specifically less exciting than the highlight reel suggests. Atlas’s halftime cameo at a FIFA World Cup match, where it delivered the ceremonial match ball, and a demonstration where it hoisted a 23-kilogram mini fridge, are the clips getting circulated. What’s actually scheduled to happen is that Atlas begins work at Hyundai’s Metaplant in Savannah, Georgia in 2028, and its job will be parts sequencing, industry shorthand for kitting: pulling the correct parts in the correct order and handing them to the line exactly when a station needs them. It’s a job that has almost nothing to do with dexterity for a highlight reel and everything to do with never being wrong. A single mis-sequenced part can stop an entire assembly line, and stopped lines are the most expensive minutes in a factory’s day. Hyundai isn’t putting Atlas anywhere near actual vehicle assembly until 2030 at the earliest, and even that expansion is described as contingent on continued technology validation, corporate language for we’ll see.

That timeline lands awkwardly next to what’s happening with Hyundai’s own workforce. The company’s South Korean union has escalated strike activity over wages, bonuses, and job security, and union leaders have pointed directly at automation and AI investment as a threat to future hiring. Roughly 2,000 union members are expected to retire every year through 2032, and the union’s worry isn’t really about today’s headcount. It’s about whether Hyundai quietly lets attrition do the work a mass layoff never could, replacing retiring assembly workers with machines instead of new hires. Notice, too, where Atlas is actually being deployed first: a non-union plant in Georgia, not a unionized plant in Ulsan. That’s not an accident of geography. It’s a preview of where labor-adjacent automation gets tested when a company wants to avoid a fight.

Hyundai’s shares dipped about 2.1 percent on the news, which the company would likely wave off as noise matching a broader Korean market decline that day. More interesting is what some analysts flagged: full ownership removes a catalyst, a Boston Dynamics IPO, that would have forced a real, market-tested price onto the robotics unit rather than a number implied by a single option exercise. Owning 100 percent of something doesn’t automatically make it more transparent to outside investors. In this case, it arguably makes it less so.

Step back, and the real story here isn’t that a car company owns a famous robotics brand outright. Plenty of automakers have flirted with robotics divisions and moonshot subsidiaries; Hyundai itself watched its flying-taxi venture, Supernal, shrink by roughly 80 percent earlier this year. The real story is that full ownership is being sold as strategic conviction when the paperwork reads like contractual obligation, that the viral robot demos are years ahead of the unglamorous warehouse job Atlas is actually scheduled to do first, and that the loudest anxiety about robots replacing autoworkers is happening in a country where, for now, Hyundai has no plans to put one on the floor.

A robot that can hand a referee a soccer ball is not the same as a robot that can hand a technician the right bolt, in the right order, thousands of times a shift, without a single mistake. Hyundai’s own rollout plan, kitting first, assembly maybe by 2030, concedes exactly that gap. Full ownership doesn’t close it. It just means Hyundai now owns the timeline, the risk, and the bill, all by itself.